Marx has been getting a lot of media attention recently, with articles exploring his relevance in the New York Times, The New Yorker, Time Magazine, Forbes and many others. A quick search on Google trends for “was Marx right” shows a blip after the crisis but a stream of mentions since 2011.

As Marx is known as having given a powerful and substantive critique of capitalism, it’s natural that whenever it is suggested that capitalism may have endemic problems, that his name will be invoked.

Many economists, including Greenspan, were claiming that crisis was permanently a thing of the past. New Labour famously proclaimed on their advent to power in 1997 that they would put an end to the cycle of “boom and bust” capitalism, only to preside over the biggest bust since the Great Depression.

Marx’s critique, by contrast, held that in fact crisis is inherent to capitalism. With two centuries of periodic crisis it’s clear that any analysis which can claim to be predictive is going to have to account for these crises.

However, something which has not been examined very clearly is how Marx’s critique of political economy was capable of describing crisis, or of making any of the other predictions which it has done. It’s important that we take stock of the analytic tools which gave rise to these predictions so that we can evaluate if we should be using them again in order to understand our current situation.

Labour at the Core

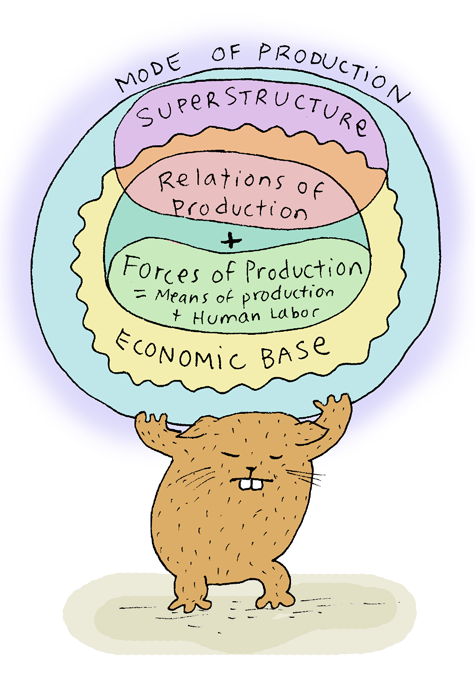

Many things in society are historically specific – they do are not time-invariant general features but arise out of particular circumstances – but some aspects of society are more permanent. In particular, one aspect of all human society thus far is that it organises human labour in order for society to continue existing.

The manner in which this labour is organised and allocated is, however, historically specific. Social organisation can be seen as arising out of competition over how to organise social labour. Because this is configured by the environment (a factor which it is important to understand includes the social organisations themselves) we can think about this as a selection process which is in many ways similar to the process of selection which life itself undergoes 1 (For a dissenting opinion, see 2).

In neolithic times organisation of labour was often done at the level of the tribe, with responsibilities being mediated through direct personal relationships.

In capitalism, by contrast, the allocation of labour happens in a deeply impersonal (but nevertheless social) way. Instead of relying on interpersonal relationships, we rely on mediation through money, in markets (For a synopsis of Marx’s Capital see 3). We try to find organisations which will pay us a wage so we can buy the things we need and want, and these organisations are responsible for allocating our labour in order to produce one or some of these commodities which are then sold on the market.

Those of us with the fortune of being successful capitalists will attempt to arrange socially useful labour by finding firms which can produce at profit, or simply invest in organisations who will do this for us.

This system is organised around a number of core features which characterise it:

- It consists of “generalised commodity production”. Capitalism requires the production of commodities for sale in a marketplace, and that this be the primary feature of social production.

- It requires “doubly free labour”. That is, a pool of wage labourers who are free to sell their labour power, and free from the capital which would be required for them to sell anything else. It makes me happy that this pun works in English as well as Germany.

- It requires finance: a system of Banking and Capital investors which can purchase requisite materials from the commodity market to fund current, or assemble new, productive endeavours.

These three aspects interlock to create the conditions for capitalism. The manner in which the general process emerges involves a large number of agents – firms, capitalists, worker, consumers.

These components are organised in what is termed a circuit of capital. Since it is in fact a circuit, a metabolic system which uses outputs as inputs to produce new outputs, there is no actual starting place – but we will arbitrarily jump on the circuit as follows:

First, money (which is obtained from prior investment by capitalists) is used to purchase commodities. These commodities are necessary precursors to some output commodity. Labour is employed in the manufacture and the product is produced for sale on the market. This process is sometimes designated as M-C-M’; that is, money is used to produce a commodity which yields more money.

All capitalists engage in this process, and the process is conducted in such a way that the difference in monies invested to monies obtained is maximised – that is, that profits are maximised.

We can write the process in a more expanded form as:

M-C1-C2-…Cn-L-M’

Where each Ci is an input commodity, and L is the amount of labour from the worker. This L, the labour supplied by the labourer can further divided into two pieces, W (wages) and S (surplus).

If we think of the process in terms of labour, we have some number of hours which are employed in the creation of the commodity C. Each of the commodities that go in as precursors to the production of commodity C, (C1…Cn) similarly had some labour time which was expended in their manufacture. Each, in turn, will have had labour and commodities which involved labour time in their manufacture. If we carry on this investigation into the labour expenditures recursively we arrive finally at total amount of labour expended in the production of a commodity. In this way a good can be reduced to pure labour content.

The central hypothesis of the LTV is that this commodity’s price is related (but not identical) to its labour content. It may be above or below but capitalist competition will have a tendency to move both towards value by giving insufficient returns to those who price below, and allowing competitors to undercut those who price too far above.

Since the system is always in motion we don’t expect these ever to coincide – even in the long run, but neither are they without constraint.

We can imagine it as similar to the concept of temperature of a gas, and the velocities of the particles of a gas. At a given temperature you can find a molecule that has virtually any velocity – but the distribution of the velocities will be dictated by the temperature with a definite peak (most probable velocity region).

This dual character of the theory, which allows a separate notion of value and the price at which something exchanges gives rise to a number of very interesting and useful features. It allows us to talk about something selling above or below its value.

While at first glance the appeal of this might not be so obvious, but even mainstream pundits seem unable to control themselves when calling something “over-priced” or that something is a “speculation bubble”. To what are they referring if the value of something is precisely its price?

It also allows us to talk much more coherently about the way that rentier capitalism actually functions – the use of monopoly or absolute scarcity to appropriate value from one branch of production into some other part of the market.

Finally it gives us a way to think “the full value of Labour”. In a “price theory of price”, where everything is valued precisely at its price, there is simply no way to talk about what the labourer was contributing to production short of what they were paid to do it. That is, by eliminating a dual structure theory one immediately eliminates the possibility of something “unpaid”.

The Historical Specificity of Capitalism

Investment at interest has existed as long as history, we have reports of Sumerians investing in long distance tin trade at interest. The Italians had sophisticated trading banks by the eleventh century for insuring and obtaining capital for shipping.

Similarly, the production of commodities for exchange in the market is likewise ancient. It was present going back to the Roman era and before. Even in agrarian England prior to the rise of capitalism, doubly free labour was common in agricultural production.

The uniqueness of capitalism is not simple the constituent parts but the way in which they interact and the fact that the bulk of economic activity is organised around generalised commodity production making use of wage labour for the purpose of profit and the utilisation of capital for improvements of the productive process. It is only as this bundle – or totality of social relations that we can understand it as historically specific.

Origins

Smith4, Ricardo5, Hodgskin[Labour Defended Against the Claims of Capital, Thomas Hodgskin], Marx6 and virtually all of the classical political economists of the 19th century took an approach to understanding modern capitalism which looked at the peculiar way in which labour was allocated in capitalist society.

The Labour Theory of value arose from a fairly abstract argument by Adam Smith. He was trying to find a reason that money could be a sensible intermediary for all of the individual valuations of goods in commodity exchange. He asked how it was that I could sell one commodity and purchase another all while utilising some single unit of intermediary (a currency). He reasoned that the thing common to all commodities which allowed an equivalence was labour. From this he formulated the hypothesis that prices reflected the labour which went into the production process.

Smith was antagonistic to the view that prices merely arose from subjective valuations of individuals. To illustrate the idea he put forward the “diamond-water” paradox, to show that valuations could not be merely subjective. Subjective valuations of diamonds could not possibly exceed that of water as water is necessary to continue living, whereas the diamond was clearly utterly superfluous. How could it be that diamonds were of greater value? For Smith, the labour needed to obtain them was the solution to this apparent paradox.

Ricardo extended Smith’s theory and clarified some aspects. He also took a closer look at rent – those elements of absolute scarcity such as land which can not merely be easily extended and those which were subject to diminishing returns, as well as the questions of international trade and taxation.

Hodgskin was among the first to articulate how the LTV could be used to advance a radical critique levelled at Capital and the claims it makes on the output of the labourer which is seen most clearly in the LTV. We see Hodgskin argue against much of the argument which would later be mathematised by the Austrians in the late 19th century. Essentially making the claim that capitals supposed “contribution” is really due itself to other labourers.

Finally we have Marx’s theory of value which draws from these former economists amongst many others in order to create a very sophisticated analysis which he presents in Capital (see footnotes for a more in-depth description of Marx’s theory).

The Problem with the LTV

The apportionment of the labour added in production to capitalist and worker is really a necessary feature of the LTV for the theory to remain consistent.

Austrian economists first attempted to deal with this by arguing that the capitalist is engaged in a special form of labour in acting as the guiding entrepreneurial force which organises all of the aspects into the process of production.

Yet it is seldom case that the entrepreneur and the capitalist are necessarily present in the same individual (Jobs and Wozniak, Serge and Page, required capital investors), and even worse for the theory, a particular genius of the investor is irrelevant to the maintenance of the system of investment.

Studies have shown that investors are often as bad or worse than a random agent at making investment decisions – and yet the system continues to function as the firms which prove a failure die and the successful investment grows. So how can it be that those who have invested in the right productive endeavour can be so highly rewarded?

Of course a theory of political economy that demonstrates that one class of individuals is essentially parasitical is unlikely to be embraced enthusiastically by that class, especially when that class is the ruling class. This meant that the theory had to go, and following on some ideas in Smith, Ricardo and others dealing with the very specific question of rents and marginal land (goods which demonstrate a law of diminishing returns) von Wieser, Walras, Bohm-Bawerk and others developed a general theory called the theory of marginal utility which demonstrated once and for all that each contributor to the production process obtain precisely what their contribution deserved.

It is also the case that this theory requires diminishing returns to production, that each further employment of capital yields less effective output. This situation is very often reversed from what occurs in reality – that is it ignores economies of scale.

Finally, the notion of the contribution which capital provides in terms of physical capital which is employed in the theory makes use of a notion of the value of capital, without reference to the labour used to provide it.

We must therefore obtain a price for the capital without reference to labour. It turns out that this reasoning becomes circular – and we end up with a “price theory of price” in which prices can only make sense in terms of prices already provided coupled with an exogenous rate of profit.

Subjectivity

Marx’s approach to the Labour theory of value takes account of subjective valuations calling them “use-value”. We understand all goods which have sale in the market place as requiring that they have two features – they have a use-value and they are considered to be useful enough by an individual at a price which it sells at. There can be no sale of mud-pies which sell at their labour value as nobody wants them (though I’ve seen tourists literally purchase Moose shit in Alaska).

This subjective valuation however does not (in the long term) change the price in a significant way. If it did rise up to a high level above its value then competition would likely drive it down again, and selling below value is difficult for any length of time if one wants to stay solvent.

By contrast the various Subjective Theories of Value imagine that people define price based on their collective subjective valuations. This is perhaps most elegantly expressed in the Arrow-Debreu theory 7. This theory has enormous technical problems, including foresight of all prices of all future products ever, the need for aggregated personal preferences to remain similar in aggregate to the individual preferences (something which is mathematically absurd). But despite these mammoth problems, it has remained more popular than the LTV.

Some Notes on Misinterpretations

The LTV is a theory of the organisation of commodity production under capitalism. While it is a “totality of social relations” it is not the only way in which labour is organised.

There are families, there are community groups there are churches there are clubs there are individuals etc. All of these perform different types of work to get outcomes which are not aiming for exchange value directly. These exist in a broader context of the core of economics being capitalist and are therefore configured by them, but capitalism does not subsume them – no mode of production has subsummed all social relations (as yet – a truly totalising capitalism would be an interesting SciFi dystopia).

As such there are many realms, including house-work about which the theory says nothing. This is not because Marx, or any of the early socialists were uninterested in housework or the family, in fact their writings show this not to be true at all. Instead it’s because capitalism does not account for this labour in price. The LTV describes hour labour is apportioned only through wage labour for generalised commodity production.

In the LTV housework is like mushrooms which grow in the woods – it is treated as an external resource that is utilised but which is not commoditised. These things however can be commoditised, and in many case childcare, washing, cooking and cleaning have been increasingly commoditised over the last century. Even the reproduction of humans themselves in sperm-banks and surrogate mothers has demonstrated commoditisation.

The confusion of the purpose of the LTV has lead to calls for wages for housework and other such demands that are strikingly similar to calls for commoditisation of the sphere of activity. We should think seriously if what we want is a deepening of generalised commodity production.

Everything which is not in capitalism is organised by something else. These other bits fall into the more general model of historical materialism and the general social organisation of all labour. Part of the task of socialism is to find out how we can generate production on a basis which is not for the sole purpose of profit formation.

But who should I listen to?

But how is the innocent bystander to make sense of all this economic technicality? Wasn’t the Labour Theory of Value defeated? Can it possibly be true that there are no useful innovations since Marx? Why should we care about the LTV? Should we not do as Marx did and pursue the most developed technical theories of the economists of today?

Firstly, we should seek theories which have explanatory and predictive power. There have been quite a number of predictions which have been verified including the fact that returns to capital will tend to outstrip those to labour which eventually leads to crisis.

Further, we have good empirical evidence that the labour content does indeed reflect in prices – and comparisons to other potential “values” such as energy are nowhere close8. There are other theories of crisis that are contingent on the LTV, such as the Law of the Tendency of the Profit Rate to Fall9. Further are predictions of crisis from overproduction10 or underconsumption11.

By contrast, marginalism and the STV have no such capacity to explain price excepting by assumption making them incredibly weak theories in the predictive sense. Further they do not provide us with theories of periodic crisis except to imagine that it’s caused by some “evil” (often state, cartel or monopoly) intervention or distortion. It’s actually quite hard to see what they do provide other than a normative theory justifying returns to capital.

The problems or areas in which the LTV is not much use are largely problems at the fringes of the theory, many of which have technical solutions. There are also many discussions of areas that may be more problematic (The Transformation Problem12 13, General rate of profit14 15).

However, all abstractions will have some data-points which don’t fit the theory precisely because the world is more complicated than any model. It matters more how useful a theory is for prediction and explanation in the regime in which we understand it to work.

The empirical quality of the theory is very important, however the LTV enjoys another importance. The labour theory of value puts labour, the human activity for our own reproduction at the centre. It is therefore a human theory and a theory which explains the world from the vantage point of those who work for a wage under capitalism.

Marx’s investigations in Historical materialism gave rise to the hypothesis that in capitalism the working class is the class which is most capable of being able to take over the productive apparatus and run it in its own interests, thereby abolishing the need for a ruling class. Hence a theory which looks at economics from the vantage point of workers is an important weapon in the arsenal.

Historically we have rarely seen any class which developed so much power and influence over society and was also subaltern. That appears to be slipping now due to the innovations of neo-liberalism, but perhaps this is not inevitable.

In terms of the most advanced economic theories of today, there is truth to the need for the incorporation of new techniques. It is important to remember, however, that the neo-classical school arose specifically because the “bourgeois economists” were terrified of using the “bourgeois theory” of the LTV any longer after Capital began rising in popularity.

This is in marked contrast to the situation of modern neo-classical macroeconomics. This theory is not particularly explanatory, but it has instead been carefully built to justify the returns to capital.

Piketty, the writer of a modern tome also entitled “Capital”16, is now widely talked about in the news. In this mammoth work however he focuses primarily on the absurdity of dynasty and inheritance and appears to have difficulty rejecting the core proposition that returns to capital are justified (though he does make some forays here as well). I believe this is a result of the focus on the tools of neo-classical political economy.

There are however elements of modern economic research that can and, indeed must be adopted. Results from behavioural economics, from econophysics17, from chartalism and MMT18 for instance should be incorporated. Further, research into the LTV as a stochastic multi-agent system has barely even been started and already has very promising results and potential predictions.

Engaging in this type of research is difficult precisely for historical materialist reasons – those who raise up such theories represent a challenge to the legitimacy of the way things are run and tend to get weeded out. It is very difficult to pursue this type of research in economics. Yanis Varoufakis has a very good short work on this subject entitled: “A Most Peculiar Failure – On the dynamic mechanism by which the inescapable theoretical failures of neoclassical economics reinforce its dominance”19.

The economic platforms which might give rise to space for such theories are more likely to come out of cooperatives and unions than universities. We can already see much of the thinking and research on inequality is a result of research by the unions. If we manage to get a network of cooperatives with a political orientation then it could potentially assist in this pursuit.

- href=”http://evolution.binghamton.edu/dswilson/wp-content/uploads/2010/01/CDPS.pdf”>Multilevel Selection Theory, M Van Vugt ▲

- href=”http://www.stephenjaygould.org/library/dawkins_replicators.html”>Replicators and Vehicles, Richard Dawkins ▲

- href=”http://www.polyluxmarx.de/fileadmin/assets/pdf/IH_PolyluxMarx_engl_WEB.pdf”>A Capital Workbook in Slides, Rosa Luxemburg Stiftung ▲

- href=”http://www.gutenberg.org/files/3300/3300-h/3300-h.htm”>An Inquiry into the Nature and Causes of the Wealth of Nations, Adam Smith ▲

- href=”http://www.marxists.org/reference/subject/economics/ricardo/tax/”>On the Principles of Political Economy and Taxation, David Ricardo ▲

- href=”https://www.marxists.org/archive/marx/works/1867-c1/”>Capital, A Critique of Political Economy, Karl Marx ▲

- href=”http://cowles.econ.yale.edu/P/cm/m17/m17-all.pdf”>Theory of Value, Gerard Debreu ▲

- href=”http://www.dcs.gla.ac.uk/~wpc/reports/metric/metric.pdf”>Value’s Law, Value’s Metric, P Cockshott, A Cottrell ▲

- href=”http://scholarworks.umass.edu/cgi/viewcontent.cgi?article=1098&context=econ_workingpaper”>Is there a tendency for the rate of profit to fall?, Deepankar Basu, Panayiotis T. Manolakos ▲

- href=”http://krieger.jhu.edu/arrighi/wp-content/uploads/sites/29/2012/08/2003_Arrighi_Towards_Theory_Captialist_Crisis.pdf”>Towards a Theory of Capitalist Crisis, G Arrighi ▲

- href=”http://www.marxists.org/archive/luxemburg/1913/accumulation-capital/”>The Accumulation of Capital, Rosa Luxemburg ▲

- href=”http://ge.tt/3TGxewe1/v/0?c”>Marx after Steedman, Bruce Roberts ▲

- href=”http://akliman.squarespace.com/writings/OSOT.doc”>One System or Two?, Andrew Kliman, Ted McGlone ▲

- href=”http://users.wfu.edu/cottrell/eea97.pdf”>The Scientific Status of the Labour Theory of Value, WP Cockshott, A Cottrell ▲

- href=”http://newleftreview.org/I/152/emmanuel-farjoun-moshe-machover-probability-economics-and-the-labour-theory-of-value”>Probability Economics and the Labour Theory of Value, Emmanuel Farjoun, Moshé Machover ▲

- href=”http://www.amazon.com/Capital-Twenty-First-Century-Thomas-Piketty/dp/067443000″>Capital in the Twenty-First Century, Thomas Piketty ▲

- href=”http://ge.tt/2XqhVJa”>Classical Econophysics, WP Cockshott, A Cottrell ▲

- href=”http://www.hetecon.net/documents/ConferencePapers/2011Non-Refereed/Mellor_AHE2011059P.pdf”>The Confusing World of Modern Monetary Theory, Mary Mellor ▲

- href=”http://uadphil.econ.uoa.gr/UA/files/1139148722..pdf”>A Most Peculiar Failure – On the dynamic mechanism by which the inescapable theoretical failures of neoclassical economics reinforce its dominance, Yanis Varoufakis ▲

Gavin is International Secretary of the Workers’ Party.